THE United States and Israel’s war with Iran is a reminder that distant geopolitical conflicts will eventually affect Malaysia.

Concerns are growing about the potential impact of the conflict on companies here.

So far, the effects have been mostly indirect, causing some pain points.

The fallout is beginning to show up in airline ticket prices, refinery operations and the government’s fuel subsidy bill.

We break down the implications by sector and industry:

Hormuz chokepoint threatens energy security

The ongoing conflict in the Middle East has paralysed the narrow Strait of Hormuz, one of the world’s most important energy corridors.

It handles roughly a quarter of global seaborne oil trade and a fifth of global liquefied natural gas (LNG) trade.

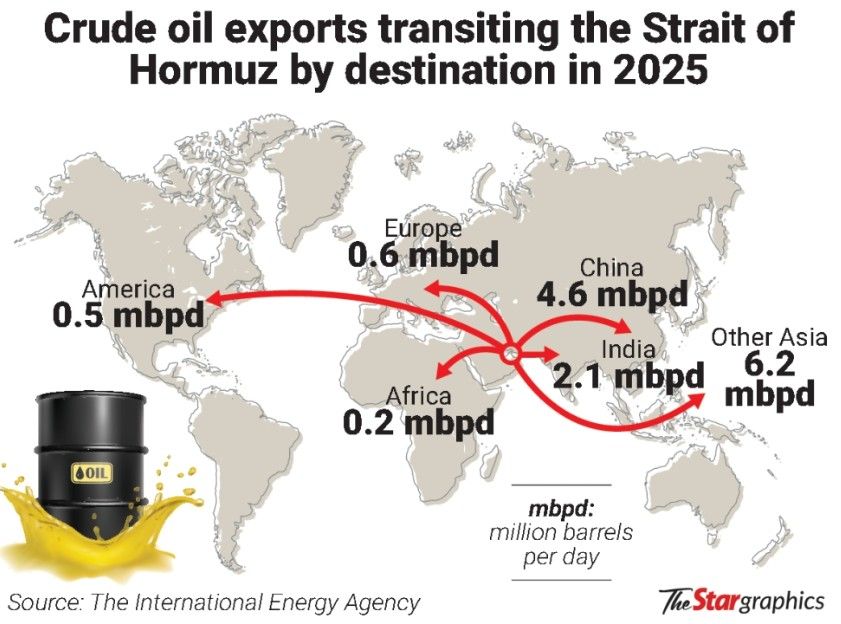

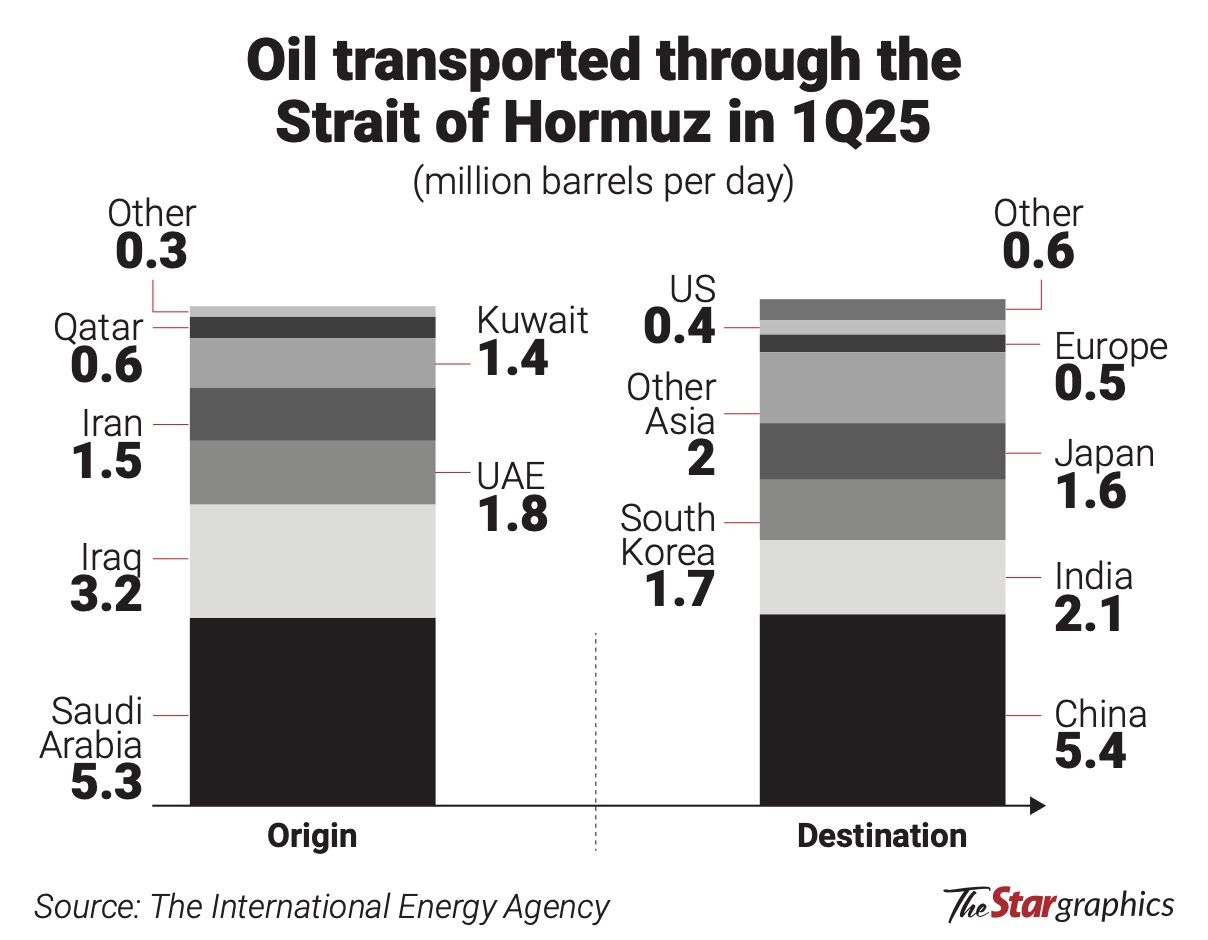

In 2025, nearly 15 million barrels per day (mbpd) of crude oil – accounting for 34% of global crude trade – and five mbpd of refined products passed through the strait, according to the International Energy Agency.

Most crude oil cargoes were destined for Asia, with China and India alone receiving 44% of shipments, while Japan and South Korea also relying heavily on the route.

Estimates suggest that, since the war began, only about a dozen tankers pass through daily – down from the usual 100 to 120.

This has raised concerns about tightening global energy supply.

SPI Asset Management managing partner Stephen Innes notes that a Group of Seven effort could release roughly 1.2 mbpd, while historically the best the system has managed is about 1.4 mbpd.

“That sounds respectable until you place it next to a disruption that could strip double-digit mbpd from the market,” he says.

He points to the near-shutdown of the Strait of Hormuz, which effectively freezes over 10 mbpd of Gulf export capacity.

“When a chokepoint like Hormuz tightens, the system does not need symbolic barrels. It needs moving barrels.

“Until the flow through Hormuz resumes, the oil market will continue to trade like a system missing its heartbeat.”

Regional risks vary.

Nomura Research believes Thailand, South Korea and India are among the most exposed – both via price and volume effects – due to their high net imports from the Middle East.

Australia, New Zealand, Indonesia and Malaysia are deemed among the least vulnerable.

The research house says Asia as a whole has roughly a month of oil inventories to tide over disruptions, while alternative routes and energy sources are not unlikely to fully offset losses from the Gulf region.

For Malaysia, the direct impact is relatively mild.

In fact, Nomura Research says the country may be one of the few net beneficiaries due to its status as a net energy exporter.

“While Malaysia is a small net crude oil importer, it has become a small net exporter of petroleum products (with an even larger surplus if we add LNG net exports).

“So, we believe the impact of rising crude oil prices on the current account balance has also turned positive, even if minimal,” it says.

“On the fiscal front, higher oil prices will increase government revenues, but we expect a proportionate increase in expenditure, as RON95 prices remain subsidised, resulting in a neutral impact on the fiscal deficit,” it adds.

Malaysia imports 68.8% of its crude oil and 12.6% of refined petroleum from the Middle East, according to Nomura Research.

The disruption of the energy supply chain is affecting feedstock supplies for petrochemical producers.

With shortages and price spikes in naphtha, LNG, and liquefied petroleum gas, analysts warn this could squeeze production, raise costs, and weigh on profitability.

CGS International (CGSI) Research says the disruption is likely to have “a negative financial and operational impact on petrochemical companies dependent on these feedstocks for production”.

“In the short term, they may not be able to secure sufficient feedstock to continue at the same operating rates after their inventories of feedstock are fully drawn down, and may have to dial down their plant utilisation rates thereafter,” it adds.

Looking ahead, the impact on petrochemical selling prices could intensify if the war continues.

CGSI Research, citing consultancy Chemical Market Analytics (CMA), notes that a prolonged conflict causing major disruptions to hydrocarbon markets and a sustained closure of the Strait of Hormuz could push petrochemical prices to rise in a “parabolic” manner.

Similarly, Macquarie Research says downstream petrochemical producers are vulnerable to price volatility, particularly those relying on naphtha.

“Chemicals, thematically, are vulnerable to heightened volatility as we see demand destruction (with end customers deferring spending),” it notes.

Within Asean, Macquarie Research sees PETRONAS Chemicals Group Bhd (PetChem) as best positioned, given its sizeable exposure to fertilisers (40% of earnings), which should benefit from strong pricing support.

The research house estimates that every US$10 per tonne increase in fertiliser prices could add RM200mil to PetChem’s earnings before interest, taxes, depreciation and amortisation, equivalent to about 3% to 4% of its normalised earnings.

CGSI Research also sees PetChem as a beneficiary, as it sources most of its gas feedstocks domestically and has limited reliance on foreign supplies.

Any negative impact would likely be confined to its Pengerang plants under Pengerang Petrochemical Co Sdn Bhd, its 50:50 joint venture with Aramco, due to potential crude import shortages and higher feedstock costs.

More broadly, citing CMA, CGSI Research notes that Asian refineries and naphtha crackers have already cut run rates due to crude supply shortages.

However, converters (buyers) may resist passing higher costs on to end customers.

“We think buyers will not agree to the price increases necessary to make production viable, and this could result in a 20% to 25% reduction in both production and demand over six to 12 months,” the research house says, adding that high-cost naphtha-based producers may have to cut back operating rates or even shut down entirely.

“As a result, actual selling price increases of petrochemical products may lag the rise in feedstock costs.”

In line with this, CMA expects producers to reduce operating rates or shut down plants, projecting a 20% to 25% decline in petrochemical output and demand over the next six to 12 months.

Tech faces currency boost, liquidity strain

While the Middle East conflict is primarily an energy story, its ripple effects are being felt across other sectors, including technology.

Tradeview Capital chief executive officer Ng Zhu Hann says the technology sector is particularly sensitive to movements in the ringgit against the US dollar, as a significant portion of Malaysian electrical and electronics (E&E) companies’ export revenue is tied to US demand.

“When oil prices surge, the ringgit typically weakens against the US dollar because of petrodollar dynamics,” he says.

“In that situation, Malaysian technology companies actually benefit because their earnings are largely denominated in US dollars.”

The petrodollar effect refers to the tendency for global demand for US dollars to rise when oil prices increase, given that crude is traded in the currency.

This usually strengthens the US dollar and weakens emerging market currencies like the ringgit.

However, the opposite could occur if geopolitical tensions ease.

“If the conflict settles and oil prices normalise, the ringgit may continue strengthening, especially if the US Federal Reserve (Fed) proceeds with rate cuts,” Ng notes.

“A weaker US dollar would then reduce the currency translation gains for Malaysian tech companies.”

Ng adds that global liquidity conditions also matter.

Elevated oil prices may fuel inflation, potentially complicating expected Fed rate cuts and limiting investment flows into technology stocks.

If rate cuts are delayed or smaller-than anticipated, there will be less liquidity in the market, he says.

“That could affect the flow of funds into the technology sector and weigh on share prices.”

Ng expects two 25-basis-point rate cuts this year, from the current 3.5% to 3.75% range.

Operationally, however, he believes the sector is relatively resilient to higher oil prices compared with heavy industries.

Malaysia’s semiconductor and E&E industry is not as energy-intensive as sectors such as petrochemicals or manufacturing.

“From that perspective, I am not too concerned about the direct impact of higher oil prices,” he says.

Nevertheless, sustained inflation could still push up indirect costs such as transportation, logistics, and supply chain expenses.

Despite these pressures, technology companies generally have the ability to pass on higher costs to customers.

“Most of the time, the key impact on the sector is not the cost side, but the currency,” Ng notes.

Another factor to watch is global technology demand.

Malaysia’s semiconductor and E&E manufacturers remain heavily dependent on orders from the United States, particularly from major technology companies.

“It ultimately depends on order flows from the US tech giants and whether their consumption slows,” Ng says.

“So far, we have not seen a direct hit.”

Although Tradeview Capital chief investment officer Nixon Wong notes impacts are mostly indirect, he says there are silver linings.

Rising geopolitical risks could make South-East Asia a more attractive investment destination for global technology firms.

“We may see fund outflows and risk-off sentiment in the short term, but in the medium term, Malaysia could benefit from supply chain diversification,” he says.

Following reports of Iranian drone attacks targeting tech infrastructure in the Gulf region, Ng says companies may increasingly look to diversify operations to safer locations.

“If anything, that could encourage more companies to invest in safer regions like Asean,” he adds.

Tourism largely unaffected, surprises possible

The tourism sector is seen as relatively resilient in the event of a prolonged US-Israel war with Iran.

Apart from arrivals from Singapore, most inbound tourists to Malaysia currently come from Asian countries including Indonesia, China, Thailand, and India.

While Singapore still accounted for the largest share last year, arrivals from other key markets are not expected to be affected by disruptions in the Middle East.

Forecasts for Singapore arrivals are also expected to remain unchanged.

Visitors from China, Indonesia, and India, who made up 9.17 million arrivals in 2025, are unlikely to be affected even if air routes through the Middle East remain disrupted, as their travel does not pass through the region.

There could, however, be an unanticipated spillover effect.

Should Asian carriers be able to step in to fill the demand gap, tourism from the Western hemisphere could increase, since the Middle East is the common transit point between East and West.

European tourists who might otherwise have transited through the Middle East may bypass the region entirely, potentially boosting arrivals into Malaysia, provided overall travel demand from Europe remains strong.

Malaysia, often seen as a “value” destination, may capture a larger share of tourists from Western countries, especially given the ringgit’s historically weak level against the US dollar and euro.

On the other hand, the country may see fewer visitors from the Middle East, who usually also travel as medical tourists.

These high-value tourists typically have longer stays, and their spending extends to hotels and high-end shopping.

Malaysia’s private medical facilities remain relatively affordable compared with Europe.

EXSIM Hospitality Bhd managing director Tan Hai Liang remains optimistic about Malaysia’s tourism outlook despite developments in the Middle East.

“Malaysia continues to stand out as one of the most attractive tourism destinations in the region.

“The country is well-positioned to capture growing travel demand as visitor arrivals and tourism activities strengthen this year in conjunction with Visit Malaysia 2026 (VM2026),” Tan tells StarBiz 7.

Based on these factors, VM2026 targets are still expected to be achievable and largely unaffected by short- or medium-term volatility arising from the conflict.