SUNWAY Bhd’s bid to take control of IJM Corp Bhd cannot be written off just yet, though admittedly, the takeover attempt is facing increasingly long odds.

The proposed deal suffered a significant setback this week after Permodalan Nasional Bhd (PNB), IJM’s second-largest shareholder, rejected the offer.

The decision came on the heels of an independent assessment by M&A Securities, which concluded that Sunway’s RM3.15-a-share offer, comprising 10% cash and 90% Sunway shares, was “not fair and not reasonable”.

That view was reinforced by a separate valuation by Rothschild & Co, which placed IJM’s indicative equity value at between RM16.81bil and RM19.72bil, or RM4.80 to RM5.63 per share.

This was at least 52% higher than what Sunway is offering. Sunway’s offer values IJM at RM11.04bil.

Chong Tjen-San, an analyst at CGS International Research, tells StarBiz 7 that Sunway had said RM3.15 a share represented its “best offer”.

“This was conveyed during the analyst briefing in late February.

“It is still early to say the deal has met a dead end. It is not over, but it doesn’t look extremely positive,” he says.

Notably, Sunway’s “best offer” remark was made before PNB announced its decision not to accept the takeover offer.

PNB, which owns about 13.5% equity interest in IJM, said its decision is based on the underlying intrinsic value of IJM shares relative to the offer price; the limited cash component of the offer; the estimated value upside of shares to be issued relative to the issue price; IJM’s dividend outlook and long term value creation potential.

This was in line with what the IJM management had reportedly said: shareholders accepting Sunway Bhd’s takeover offer could capture only about 20% of the company’s future growth upside.

Also, a key sticking point is how Sunway is offering to pay: only 10% cash, with the remainder paid via new Sunway shares.

In effect, Sunway would need to fork out only about RM1bil in cash to acquire IJM – a group with roughly RM1.9bil in cash on its balance sheet.

Some see this as unreasonable.

The ball is now in Sunway’s court.

A better offer may bring PNB back into the equation.

“PNB could be trying to get a better deal when it voiced its rejection of the offer.

“It depends on Sunway now. If it is serious about this deal and sees good prospects in IJM, Sunway could raise the offer price and increase the cash portion of the offer which is currently only 10%,” an analyst says.

PNB’s approval is key for this takeover attempt to achieve its ultimate goal, which is to privatise IJM.

To be clear, Sunway needs to obtain 50% plus one share equity interest in IJM for its takeover offer to take effect.

But to compulsorily delist IJM from the stock exchange and to take it private, Sunway needs 90% IJM shareholders’ approval – and this cannot be achieved with PNB rejecting the deal.

Chong says that Sunway has to take IJM private for the deal to be “meaningful”.

“Only then it can better extract value and drive synergies optimally.

“This may not be achievable if Sunway only gets to acquire the bare minimum of 50% plus one share in IJM.”

Now, PNB is only one of the resistance that Sunway faces in its voluntary takeover offer (VTO).

There are three other government-linked entities as major shareholders of IJM.

The Employees Provident Fund (EPF) is the single-largest shareholder with slightly over a 20% stake.

Retirement Fund Inc and Urusharta Jamaah Sdn Bhd own 9.6% and 3.7%, respectively.

Collectively, the four government-linked shareholders collectively control at least 48% of IJM.

What is uncertain now is whether these shareholders will vote along the same line.

If that is the case, PNB’s rejection is indeed a bad sign for Sunway.

An analyst tells StarBiz 7 that the government-linked shareholders may take different stands on the offer, based on the interests they serve.

“However, there is a risk for all of them to say no to the deal, not just because of the offer price, but also because of the bumiputra ownership issue being played out.

“With speculations that an early general election may be on the horizon, the government may not want to risk a sensitive issue like this,” according to the analyst.

This is not something to be brushed off easily, as politics can effectively influence whether the deal lives or dies.

Kuala Lumpur Kepong Bhd learnt this the hard way.

In 2023, politicians thwarted its plan to acquire a 33% stake in Bursa Malaysia-listed Boustead Plantations Bhd for RM1.15bil – and then to privatise the company together with Lembaga Tabung Angkatan Tentera.

In both KLK-Boustead Plantations and Sunway-IJM deals, the criticism is centred on the sale of bumiputra assets.

With IJM’s shareholding dominated by institutions that ultimately answer to public sentiment and government priorities, considerations may go beyond the intrinsic value and the offer price.

Politics aside, since Sunway’s VTO, the EPF has steadily bought more IJM shares, raising its stake from 18.3%.

With one-fifth of the share base in the EPF’s hands, the fund could press Sunway for a better deal.

Wake-up call

Whether or not the takeover goes through, the episode should serve as a wake-up call for IJM.

A source close to IJM tells StarBiz 7 that its non-executive chairman Tan Sri Krishnan Tan has long pressed management to accelerate efforts to unlock the value of the group’s assets.

“This wasn’t done fast enough. So, it is not surprising that Sunway made the offer because it sees the opportunity to extract value from IJM’s assets.”

Sunway’s takeover proposal appears to be a blessing in disguise.

IJM has highlighted three major initiatives to unlock value: listing its Malaysian and Singaporean construction assets, exiting the Indian market where it holds infrastructure and property assets, and monetising mature highway assets such as the Sungai Besi Expressway or Besraya and Kajang-Seremban Highway or Lekas.

“By remaining with IJM, shareholders retain full exposure to the company’s long-term growth potential,” IJM chief executive officer and managing director Datuk Lee Chun Fai said in a recent press briefing.

He noted that Sunway’s offer comes at the low point of IJM’s earnings cycle but at the high point of its asset value.

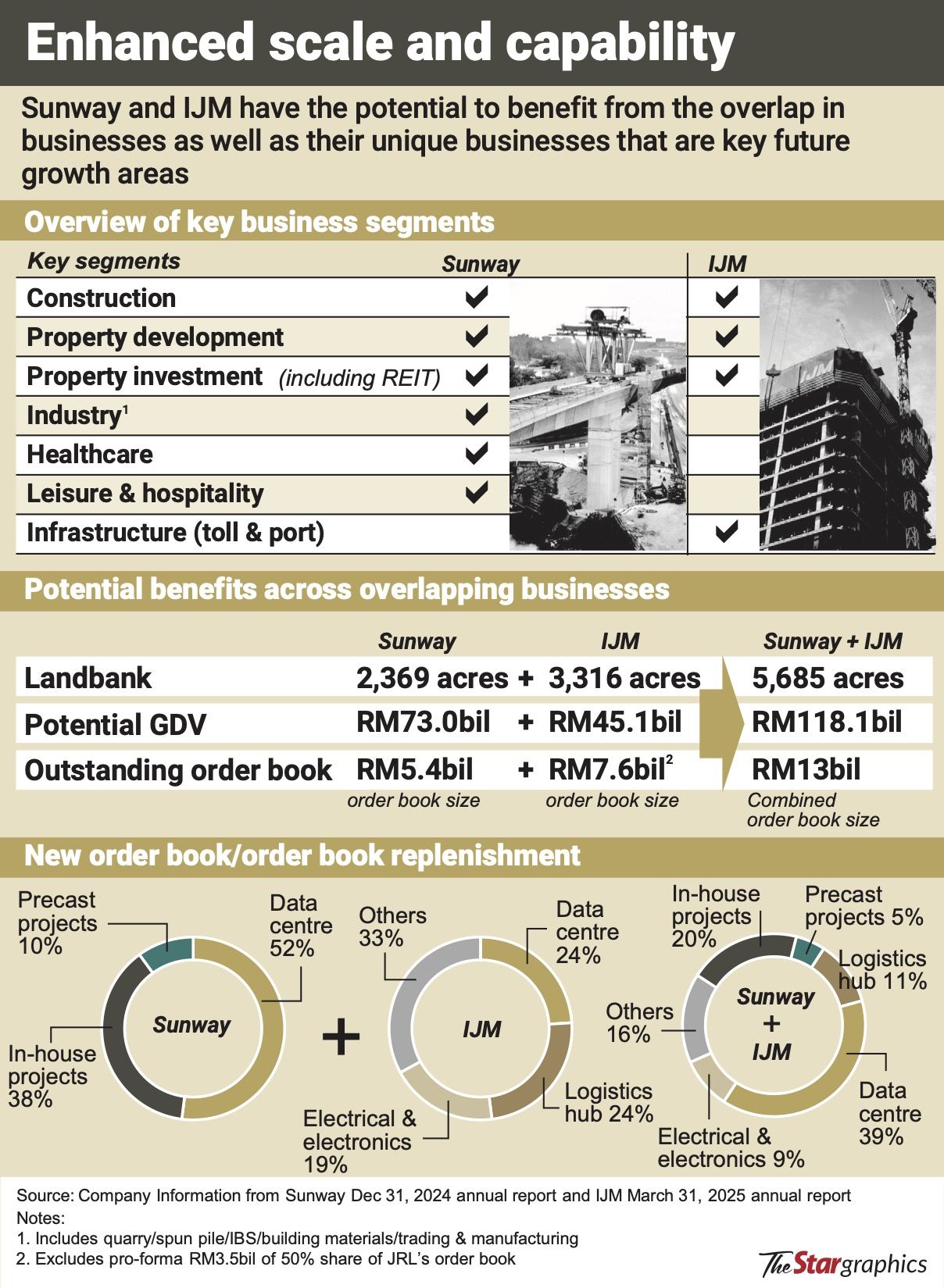

IJM has a footprint in four main segments, namely, construction, property, industry and infrastructure.

Under the construction segment, IJM has expertise in civil engineering, utility construction, building projects, along with major transport infrastructure construction.

It has also been involved in the construction of all major rail transportation networks in the Klang Valley.

In the property segment, the group develops residential, commercial and mixed use projects.

As for industry, IJM manufactures building materials such as concrete piles, ready-mix concrete and precast components.

Meanwhile, under the infrastructure segment, IJM owns and operates toll-highway concessions in Malaysia and overseas, as well as the Kuantan port – a deepwater, multi-cargo seaport.

It is, therefore, not surprising there is market interest in IJM’s assets.

A local financial news outlet previously reported that there are three or four other offers –other than Sunway – to acquire IJM.

The potential offerors mentioned were a Sarawak government-led bumiputra consortium; YTL Corp Bhd; and UEM Corp Bhd.

AFA Group is also said to be exploring options to acquire IJM’s toll concession business.

AFA, which is led by Tan Sri Azmil Khalid, is the operator of the Kuala Lumpur-Karak Highway and East Coast Expressway phase one.

The news about alternative offers are not true, a source close to IJM says.

“IJM has not received any offer so far, apart from Sunway.”

Meanwhile, another source confirmed that AFA did not make an offer to IJM.

“It was not a direct offer. If Sunway is successful in its bid, AFA wants to be considered as a buyer for IJM’s highway business.

“But that goes to any other parties looking to acquire IJM, if any,” according to the source.

In a December 2024 interview with StarBiz 7, AFA Group chairman Azmil had said he is always on the look out for “brownfield” or existing tolls.

It is also worth remembering that Malaysian Resources Corp Bhd had pursued in 2010 a merger with rival IJM Land, which at that point was listed –although majority owned by IJM Corp.

The proposed merger was later aborted as the companies could not agree on the deal’s terms and conditions.

In short, the market has always shown interest in IJM’s assets.

In the case of Sunway, the takeover of IJM will provide a boost in infrastructure expertise and the opportunity to drive synergies between the real estate businesses of IJM and Sunway.

CGSI’s Chong says that Sunway has a better track record in maximising value from its assets.

“This is reflected in its share price compared to IJM.

“If an investor wants to buy into a better managed group, albeit with a higher valuation, the Sunway offer is something for the investor to consider.”

That said, Chong also points out that holding IJM shares over the long term will be more meaningful, if IJM executes well the plan to extract best value from its assets.

Many of IJM’s assets are still in the nascent stage.

“But this really depends on the execution,” he adds.

Another veteran fund manager believes that a merger of Sunway and IJM will not only drive synergies, but also increase “investability”.

“A bigger merged entity will get the attention of large foreign funds to invest.

“Not only that, a merged Sunway-IJM could take on bigger projects both domestically and beyond Malaysia because they will have the expertise and resources.

“Also, now that Sunway’s healthcare business has been carved out following the initial public offering, Sunway’s management can better focus on extracting best value from IJM’s assets, if the deal does happen,” he says.